Income Tax Return is a form or document that individuals and entities are required to file with the Income Tax Department, providing details of their income earned during a specific financial year. It includes information about various sources of income, deductions claimed, and tax payments made.

As per the Income Tax Act, 1961, individuals and entities falling under the following categories are required to file ITR Return:

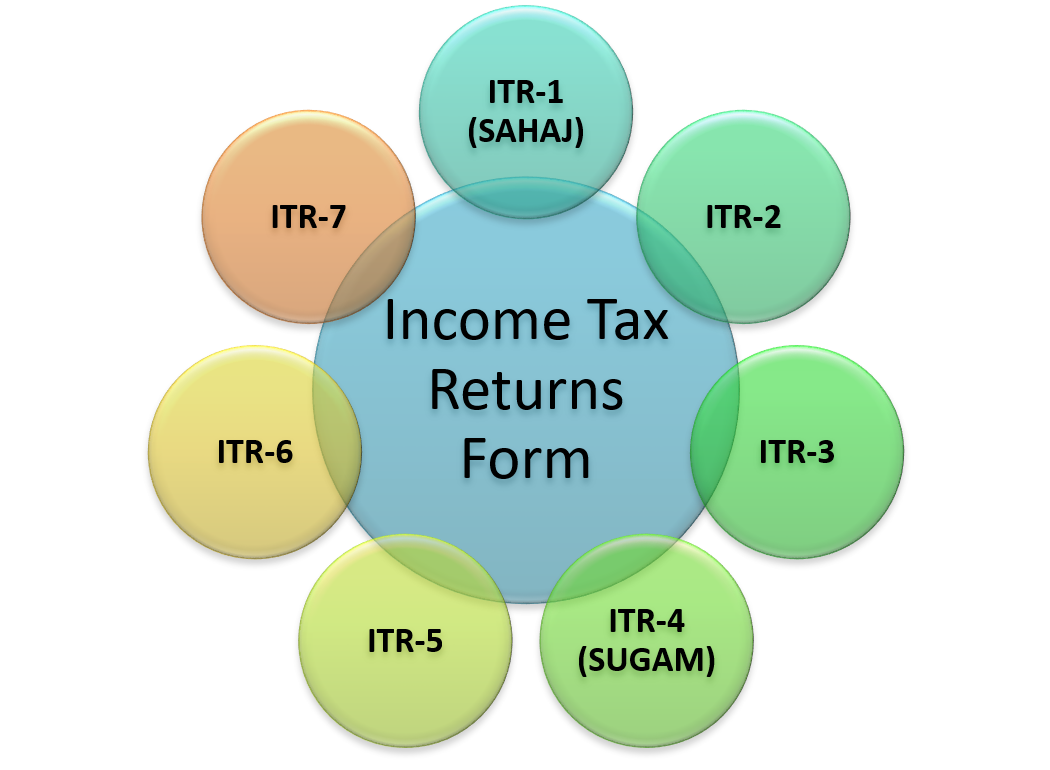

The Income Tax Department has designed different types of ITR forms to cater to various categories of taxpayers. The appropriate form depends on the nature of income, sources of income, and the taxpayer’s residential status. Some commonly used ITR forms include:

Income Tax Return Filing is an essential aspect of financial responsibility for individuals and businesses in India. It is a process through which taxpayers report their income, deductions, and tax liabilities to the government. While it may seem burdensome at times, filing income tax returns carries significant importance for both the taxpayers and the nation as a whole. The importance of ITR Filing in India are as follows:

The following are the advantages of ITR Filing in India:

One of the primary advantages of filing Income Tax Returns is to fulfill your legal obligations as a taxpayer. The Income Tax Act, 1961 mandates that individuals and businesses earning above the specified threshold file their tax returns. By complying with the law, you avoid penalties, fines, or legal complications that could arise from non-compliance.

Income Tax Return filing acts as a declaration of your income and assets to the government. It helps in establishing a clear record of your financial activities and offers transparency to tax authorities. This documentation becomes crucial in various situations, such as applying for loans, securing visas, or participating in government tenders, where your financial status may be scrutinized.

Income Tax Returns provide an opportunity to claim various tax deductions and exemptions available under the Income Tax Act. These deductions can significantly reduce your tax liability and help you save money. Popular deductions include those for investments in tax-saving instruments (e.g., Employee Provident Fund, Public Provident Fund), health insurance premiums, home loan interest payments, and contributions to charitable organizations.

Additionally, filing income tax returns enables individuals to claim refunds if they have paid excess taxes during the financial year. Tax refunds can arise from sources like TDS (Tax Deducted at Source) or advance tax payments. By filing your returns, you can receive the refund due to you from the government, providing a welcome financial boost.

Consistently filing income tax returns helps build a reliable financial history. This is particularly beneficial for individuals who plan to apply for loans or credit cards in the future. Lenders assess the creditworthiness of applicants based on their income tax return filings, making it essential to have a clean and consistent record. A positive financial history increases the likelihood of getting favorable loan terms, higher credit limits, and lower interest rates.

The Income Tax Department scrutinizes cases where individuals or businesses have not filed their tax returns or where discrepancies are detected. By filing your returns promptly and accurately, you minimize the chances of attracting the attention of the tax authorities for the wrong reasons. Proactive compliance reduces the risk of being subjected to income tax audits, notices, or investigations.

Filing income tax returns requires individuals to compile and organize their financial information. This process encourages better financial planning and budgeting. By evaluating your income, expenses, investments, and savings, you gain a comprehensive understanding of your financial standing. It allows you to identify areas for improvement, make informed decisions, and optimize your financial resources effectively.

Filing income tax returns is a fundamental way to contribute to the development and progress of the nation. Income tax revenue forms a significant part of the government’s income, which is utilized for infrastructure development, social welfare programs, education, healthcare, defense, and more. By fulfilling your tax obligations, you actively participate in the nation-building process and help create a better society for all.

To complete the income tax return filing process accurately and efficiently, it is essential to gather and organize the necessary documents. The following are the documents required for ITR Filing:

The first step in filing your income tax return is to determine the appropriate form to use. The Income Tax Department of India provides several forms for different types of taxpayers, such as individuals, Hindu Undivided Families (HUFs), companies, and partnerships. The commonly used forms for individuals are ITR-1 (Sahaj), ITR-2, ITR-3, and ITR-4. Carefully assess your sources of income and choose the form that suits your situation.

Before starting the income tax return filing process, gather all the necessary documents. These may include your PAN (Permanent Account Number) card, Aadhaar card, bank statements, Form 16 (provided by your employer), Form 16A (for income from other sources), details of investments, and any other relevant financial documents. Having these documents readily available will help you provide accurate information while filing your return.

The next step is to compute your total income for the financial year. Consider all sources of income, such as salary, house property, capital gains, business or profession, and other incomes. Deduct eligible expenses, deductions, exemptions, and allowances to arrive at your taxable income. Use the income tax slabs and rates applicable for the financial year to calculate your tax liability accurately.

The Income Tax Department has made it mandatory for most taxpayers to file their income tax returns online. Visit the official website of the Income Tax Department (https://www.incometaxindiaefiling.gov.in) and register yourself as a taxpayer. Once registered, log in to your account and select the relevant income tax return form. Fill in the necessary details, such as personal information, income details, and deductions. Double-check the information provided before submitting the return.

After filling in the required details, verify your income tax return. The Income Tax Department provides multiple verification methods, such as using Aadhaar OTP (One-Time Password), generating and sending a signed physical copy of ITR-V to the Centralized Processing Centre (CPC), or using Electronic Verification Code (EVC). Choose the verification method that suits you and complete the verification process.

After successfully filing your income tax return, ensure that you keep a copy of the filed return for future reference. It is advisable to retain copies of Form 16, Form 16A, and any other relevant documents supporting the information provided in your return. These documents may be required for audit purposes or while applying for loans or visas.

If, after filing your return, you find that you have a tax liability, make the payment as per the guidelines provided by the Income Tax Department. Utilize the authorized modes of payment, such as net banking or debit/credit card, to pay the outstanding tax amount. Remember to pay any due taxes before the specified due dates to avoid penalties and interest charges.

In some cases, the Income Tax Department may send a notice seeking additional information or clarification regarding your income tax return. If you receive such a notice, respond promptly and provide the requested details. Ignoring or delaying the response may lead to further complications, including penalties.

The Income tax filing due dates for FY 2023-24 (AY 2024-25) are as follows:

Sr. No. | Category of the Tax Payer | Income Tax Filing deadlines for the FY 2023-24 (AY 2024-25) |

1. | Individual / HUF / AOP / BOI (no need for audited books of accounts) | 31st July 2024 |

2. | Businesses (With Audit) | 31st October 2024 |

3. | Businesses that require transfer pricing reports (for international/specified domestic transactions) | 30th November 2024 |

4. | Return Revised | 31 December 2024 |

5. | Late Return | 31 December 2024 |

The following are the penalty may be imposed on taxpayer in case of late income tax return filing:

Section 234F was introduced in the Income Tax Act, 1961, in order to encourage timely filing of income tax returns. According to this section, if an individual or Hindu Undivided Family (HUF) fails to furnish the income tax return within the specified due date, they are liable to pay a late filing fee. The applicable fees under Section 234F are as follows:

However, there is a relief provision for small taxpayers. If the total income of the individual does not exceed Rs. 5, 00,000, the maximum fee payable is restricted to Rs. 1,000.

It is important to note that the late filing fee under Section 234F is not applicable to individuals who are 80 years or older at any time during the relevant financial year.

Apart from the late filing fees, the Income Tax Act, 1961, also imposes interest on delayed payment of taxes. If the taxpayer fails to pay the income tax liability within the due date, they will be liable to pay interest under Section 234A, 234B, and 234C of the Act. Let’s understand these sections in detail:

Under Section 234A, if a taxpayer fails to file the income tax return within the due date, they are liable to pay interest at the rate of 1% per month or part thereof. This interest is calculated from the due date of filing the return until the actual date of filing.

If a taxpayer fails to pay the advance tax or pays an amount less than the required installment, they will be liable to pay interest under Section 234B. The interest rate is 1% per month or part thereof, calculated from the due date of advance tax installment until the actual payment of tax.

Section 234C applies to individuals who are liable to pay advance tax in installments. If the taxpayer fails to pay the required installment or pays an amount less than the prescribed percentage, they will be liable to pay interest under Section 234C. The interest is calculated at the rate of 1% per month or part thereof for the period of default.

Apart from the penalties mentioned above, the Income Tax Act, 1961, also includes provisions for prosecution and other consequences in case of willful non-compliance or fraud. If a taxpayer willfully fails to furnish the income tax return or provides false information, they may face legal action, which could include prosecution, imprisonment, or both, along with the imposition of penalties.

It is important for taxpayers to understand their obligations under the Income Tax Act, 1961, and adhere to the specified timelines for filing income tax returns. Timely compliance not only helps avoid penalties but also ensures a smooth tax filing process and maintains the integrity of the taxation system.

In conclusion, ITR filing is a crucial responsibility for individuals and entities in India. By understanding the process, gathering the necessary documents, computing income and tax liability accurately, and adhering to the deadlines, taxpayers can fulfill their obligations effectively. It is advisable to stay updated with the latest rules and guidelines issued by the Income Tax Department to ensure compliance and avoid any penalties or legal issues.

Copyright © 2024 Goyal Mangal & Company. All Rights Reserved