| Content

Taxable in case of all employees: |

WHAT IS SALARY?

The term salary under INCOME TAX ACT, 1961 includes both monetary payments (i.e. basic salary, dearness allowance, bonus, pension, commission, allowances, etc.) as well as non-monetary facilities (i.e. vehicle provided by company for personal work, housing accommodation, medical facility, interest free loans, etc.

In this article we will learn in brief about tax treatment of allowances and perquisites, the main components while calculating the taxable income from the head salary.

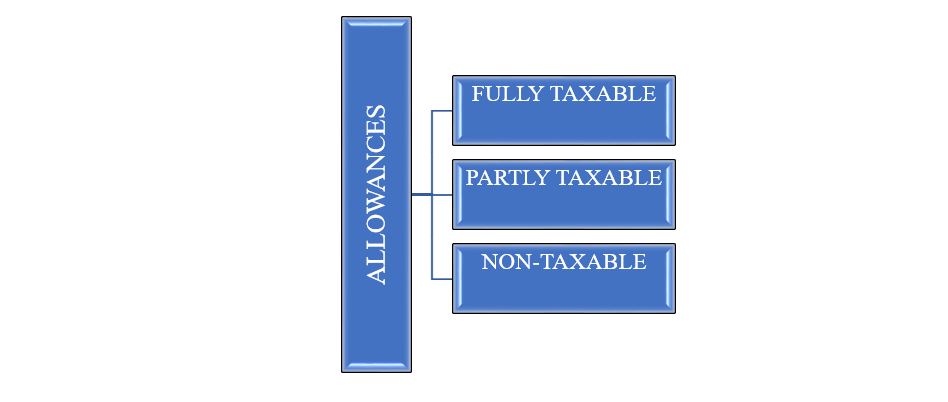

ALLOWANCES

Generally allowances are given by employers to their employees to meet some particular daily life requirements such as House rent, uniform expenses, conveyance, etc.

As according to INCOME TAX ACT, 1961 allowances are classified into three categories:

| Taxable Allowances | Partially-Taxable allowances | Non-Taxable allowances |

|

|

|

PERQUISITES

The term perquisites indicate some extra benefit in addition to amount may be legally due by way of contract for service rendered. Perquisites may be in cash or in kind.

Perquisites can be classified in three ways:

TAXABLE IN CASE OF ALL EMPLOYEES:

- Rent free accommodation.

- Concession in rent.

- Payment made by employer against the obligation of employee.

- Amount payable directly or indirectly by the employer for assurance of life of assesse

- Specified security or Sweet equity shares allotted or transferred by the employer.

- Any amount paid into contribution to an approved superannuation fund.

- Any other fringe benefit and amenity

EXEMPT IN CASE OF ALL EMPLOYEES:

- Leave travel concession subject to if only the actual amount spent

- Medical Facilities & Reimbursements

- Computer or Laptop provided for official or personal use

- Initial fees paid for corporate membership

- Refreshment provided to employees during working hours in the office premises

- Payment of amount of annual premium on personal accident policy

- Subscription to periodicals and journals required for the discharge of work

- Provision of Medical Facilities

- Gifts not exceeding Rs. 5000 per annum

- Use of health club and sports facility

- Child Education Allowance (Rs.100 per month. per child – max. 2 children)

- Hostel Allowance (Rs. 300 per month per child – max. 2 children) is exempt.

- Transport Allowance: Rs. 800 per month – Rs.1600 per month. (If handicapped)

- Free meal provided by company during work hours or through paid non-transferable vouchers not exceeding amount 50 Rs. per meal or free meal provided during work hours in a remote area.

TAXABLE IN HANDS OF SPECIFIED EMOPLOYEES

An employee is said to be a specified employee in any of the following cases: If he is director of the company; or he has any substantial interest in the affairs of the company. (Substantial interest means that the employee holds at least 20% of the voting power (equity shares) in the company); or Employee is earning monetary income i.e. more than 50,000 p.a.

It includes the following:

- Motor car given by company to employee

- Motor car owned by employee but the expenses will reimbursed by employer

- Two wheeler owned by employee but the expenses will reimbursed by employer

- RFA and accommodation at concessional rate.

- Security or shares provided by ESOP.

- Leave travel concession.