Every tax system advises firms on methods to comply with laws. Firms must submit returns on time, pay taxes regularly, and retain records under a tax system. Small business owners lack the knowledge and expertise to comply with such regulatory obligations. Small enterprises can pay a composition charge. This increases compliance without the hassle of document storage. The Goods and Services Tax (GST) (One Nation One Tax Scheme) aims to unify indirect taxes into one tax and give a composition scheme for small businesses. The GST Composition Scheme simplifies tax compliance for eligible enterprises.

What is GST Composition Scheme?

The Composition Scheme is a simple and easy scheme under the Goods and Services Tax (GST) for taxpayers with an aggregate annual turnover of less than Rs. 1.5 crore. The scheme is designed to reduce the GST formalities for small taxpayers and allows them to pay GST at a fixed rate of turnover. Scheme is designed for small businesses that are unable to keep meticulous records and account books. GST composition scheme turnover limit 2022-23 is below 1.5 crores/75 Lakhs.

To make GST compliance simple for small businesses, the government introduced the option to use the composition scheme. No ITC is provided, and the assessee must pay output tax at the lowest rate, according to the Scheme. Additionally, the assesee must submit quarterly and annual returns rather than monthly returns.

Key features of Composition Scheme

The following are some of the primary GST composition scheme’s rules:

- Eligibility: This scheme is not open to everyone. It is only for taxpayers whose aggregate turnover does not exceed Rs. 1.5 crore/75 lakh in a financial year so it is GST composition scheme limit.

- Rate of Taxation: The recommended tax rate under scheme will be less than the standard GST rate but not less than 1% of the turnover throughout the financial year. The GST composition scheme’s tax rates are predicted to range between 1% and 3% individually. Rate of GST for Manufacturers & Traders of Goods is 1% of turnover. Restaurant Owners is 5% of Turnover and Service Providers is 6% of turnover.

- Not eligible for Input Tax Credit: According to section 16, products, and services on which the Composition Tax (under section 8) has been paid do not qualify for the Input Tax Credit in GST.

- Intrastate supplies: This scheme is only available to local suppliers, i.e., those who provide within a state. Interstate suppliers will be subject to standard GST legislation.

- Voluntary Application: For GST Composition Scheme benefits, taxpayers must voluntarily register annually. The taxpayer would be shifted to a regular program if his turnover exceeds Rs. 75 lakh/1.5 crores. All VAT Composition Scheme taxpayers must voluntarily enrol for this scheme.

- Quarterly/Yearly Return: Instead of filing 3-4 returns monthly, taxpayers registered under this program will just have to file one return every quarter and a yearly return.

- Bill of Supply: This plan requires taxpayers to submit a bill of supply instead of a tax invoice.

- Penalty: If a taxable person is ineligible for this plan, the tax authorities can issue a penalty equal to his tax burden. Thus, choosing this strategy and paying taxes requires caution.

Advantages of Composition Scheme

The following are the advantages of registering under composition scheme:

- Less compliance (with filing returns, keeping books of records, and sending out bills).

- Tax exposure is limited.

- High liquidity because of low taxes.

Disadvantages of Composition Scheme

Registering under GST composition scheme has certain drawbacks:

- Limited business territory. The dealer cannot transact interstate.

- No Input Tax Credit for composition traders.

- GST-exempt goods such as alcohol and e-commerce goods cannot be sold by the taxpayer.

However, In the recent budget, intrastate E-Commerce Operator sellers can choose composition under certain conditions. The law will be changed after notification (notification forthcoming).

Conditions to be satisfied to opt for composition scheme

To choose a composition scheme, the following conditions must be met:

- A dealer who chooses the composition plan cannot claim an Input Tax Credit under GST.

- The merchant cannot sell commodities that are not subject to GST, such as alcohol.

- For transactions involving the Reverse Charge Mechanism, the taxpayer must pay tax at regular rates.

- If a taxable person operates many enterprises (such as textiles, electrical accessories, groceries, and so on) under the same PAN, they must register all of them under the system collectively or opt out of it.

- The taxpayer must include the phrase ‘composition taxable person’ on every notice or signboard conspicuously placed at their place of business.

- The taxpayer must include the phrase ‘composition taxable person’ on every bill of supply he issues.

- According to the CGST (Amendment) Act of 2018, a producer or trader can now additionally supply services up to 10% of sales or Rs.5 lakhs, whichever is greater.

Who is eligible for the GST Composition Scheme?

Composition Scheme is available to small taxpayers having an annual turnover of up to Rs. 1.5 crore. The composition scheme is open to manufacturers, restaurants, and retailers with a turnover of less than Rs1.5 crore. Those who provide goods and services (not exceeding Rs.5 lakhs in total) may choose the composition scheme.

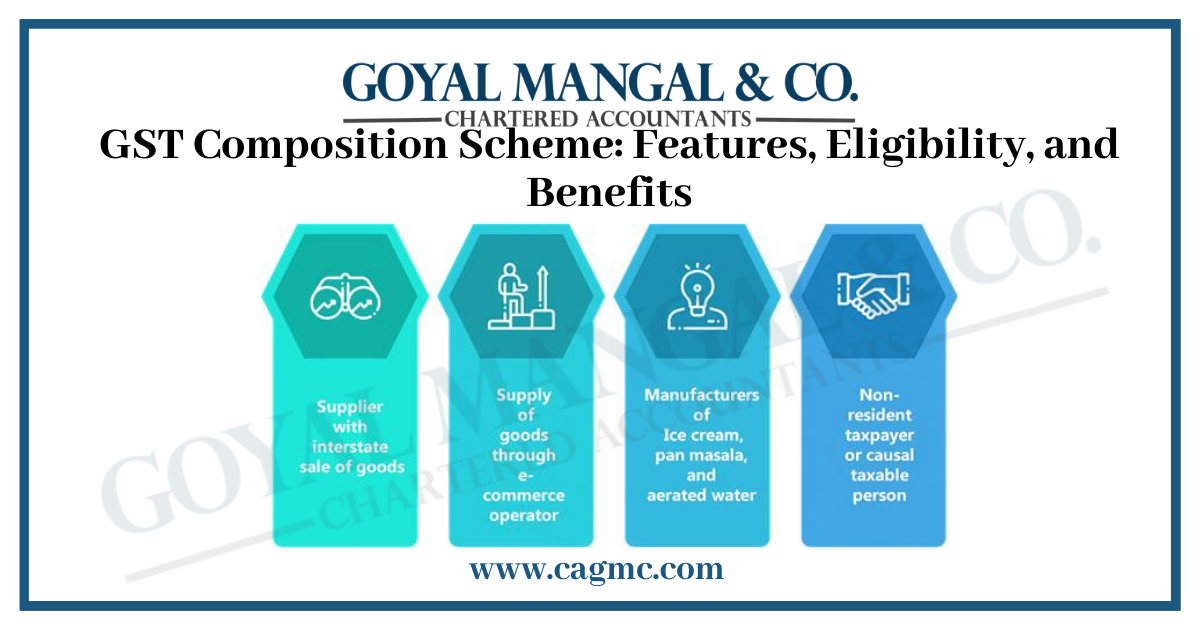

Who is not eligible for the GST Composition Scheme?

All mentioned below are the ones who are in – eligible for composition scheme:

- A company with a turnover of more than Rs. 1.5 crore/75 lakh.

- A taxable person who is in the business of delivering services.

- A person who makes an interstate outward supply of goods is taxable.

- A taxable person is someone who makes a supply through an E-commerce operator. In the recent budget, intrastate E-Commerce Operator sellers can choose composition under certain conditions. The law will be changed after notification (notification forthcoming).

- A taxable person is someone who makes a supply of products that are not subject to taxation, such as alcohol, gasoline, and diesel.

- Taxable individual who works in the service industry, manufactures pan masala, ice cream, tobacco, and tobacco replacements.

GST Composition Scheme Registration

Any current taxpayer who is not enrolled in the Composition Scheme may opt in (subject to qualification) beginning with the start of the next financial year. For composition scheme registration the application must be submitted on or before March 31st of the previous year for the returns to be filed on time.

Dealers under the Composition plan may be able to switch to a regular plan at any time during the year if they so desire. They cannot, however, convert back to the Composition Scheme during the same Financial Year.

Restrictions imposed by the GST Scheme of Composition

Following are the restrictions under composition scheme:

- The composition dealer is not required to collect tax from the service recipient.

- Composition Dealers are not permitted to claim GST input tax credit (ITC) on purchases.

- A composition merchant may not make interstate outbound supplies, but he may make interstate inward supplies.

- A tax invoice cannot be issued by a composition dealer; instead, a bill of supply must be issued.

Composition scheme to Regular Scheme

When a taxable person who was paying tax under the GST composing scheme begins paying tax under the standard Scheme, he or she is eligible for the Input Tax Credit. Such a person may claim input tax credit for the following products held on the day immediately preceding the day on which he becomes obliged to pay tax under the usual plan.

Inputs kept on stock, Inputs contained in semi-finished or finished goods held in stock, as reduced by such percentage points as may be prescribed ITC shall, however, not be available in respect of supplies of goods/services to him after the expiry of one year from the date of issue of the tax invoice relating thereto calculated in the prescribed manner.

Transition from a Normal Dealer to A Composition Dealer

According to section 16(12) of the GST Law, when a taxpayer liable to pay tax as a regular taxable person switches over to paying tax under section 8 (GST Composition Scheme), he must debit the electronic credit/cash ledger equivalent to the Input Tax Credit in respect of inputs held in stock and inputs contained in semi-finished and finished goods held in stock as on the day immediately before the switch.

Eligible and ineligible input tax credit under Composition Scheme.

Businesses cannot claim input tax credits (ITC) on their purchases under India’s GST Composition Scheme. As a result, they are unable to use the tax paid on inputs as a credit against the tax owed on their supplies. As a result, the ITC availability is restricted for taxpayers registered under the Composition Scheme.

- ITC for pre-GST stock: If they have the relevant tax invoices, taxpayers registered in the Composition Scheme are allowed to claim input tax credits on the qualifying stock of products acquired prior to the implementation of the GST.

- Input tax credit on purchases: Under the Composition Scheme, taxpayers are not permitted to claim an input tax credit on purchases they make for their business operations. This comprises products and services utilized in production, trade, or service provision.

- Input tax credit on interstate purchases: Under the Composition Scheme, businesses are not entitled to get ITC on items bought from other states or Union Territories.

- ITC on exempt supplies: A Composition Scheme taxpayer who makes exempt supplies (i.e., services that are not subject to GST) is not entitled to an ITC on the inputs used to make such services.

Reversal of Input Tax Credit

Input Tax Credit is reversed if the taxable person converts from the Regular Scheme to the GST Composition Scheme. When a person who has used ITC switches to the composition scheme, he must pay an amount equivalent to ITC in respect of the goods on the day immediately preceding the date of such switch over (calculated in the prescribed manner) by debit in the electronic ledger or the cash ledger.

Inputs kept in stock, Inputs contained in semi-finished or finished items held in stock, as reduced by the prescribed percentage points, and capital goods The balance of input tax credit remaining in the credit ledger after payment of such amount shall lapse.

What are the returns that a composition dealer must file?

A dealer must pay tax in a quarterly statement CMP-08 by the 18th of the month following the end of the quarter. From FY 2019-20 onwards, a return in form GSTR-4 must be filed yearly by the 30th of April of the next fiscal year.

GSTR-9A is an annual return that must be filed by December 31st of the following fiscal year. It was waived for fiscal years 2017-18 and 2019-20. Also, a dealer registered under the composition system is not required to keep extensive records.

Reduced late fees for GST returns

When a GST return is filed beyond the due date, a late fee is assessed. The government has lowered the late costs for GSTR-1, GSTR-3B, GSTR-4, GSTR-5, GSTR-5A, and GSTR-6 as follows (late fees will stay the same until future notifications).

- Normal Return (GSTR-1, GSTR-3B, GSTR-4, GSTR-5, GSTR-5A and GSTR-6) – Rs 50 per day of delay

- Nil Return (GSTR-1, GSTR-3B, GSTR-4, GSTR-5 and GSTR-5A) – Rs 20 per day of delay.

The maximum late fee allowed is Rs. 5000. From July to September 2017, the government reduced late fees for GSTR-3B. Any late fees paid for these months will be reimbursed back to the Electronic Cash Ledger under the Tax category. This can later be used to settle your GST liability.

GST form for Composition Scheme

A person who is part of the Composition Scheme needs to file the following GST Forms:

- GST CMP-02: This form must be filled out when the Composition Scheme is chosen.

- GST CMP-03: The user must fill out this form if they want to leave the Composition Scheme.

- GST CMP-04: You need to fill out this form if you want to change any of the information you gave when you signed up for the Composition Scheme.

- GST CMP-05: This form needs to be filled out if a person who pays taxes is no longer qualified for the Composition Scheme. It needs to be sent to the tax authorities.

- GST CMP-06: The user must fill out this form to pay taxes through the Composition Scheme.

Takeaway

With a turnover of up to Rs. 1.5 crore, small enterprises and service providers can take advantage of the Composition Scheme under the CGST Act, a simplified tax scheme. This plan facilitates GST compliance by lowering the compliance costs for small taxpayers. Each type of taxpayer has a unique composition tax rate and GST forms. Before deciding to participate in the Composition Scheme, small enterprises and service providers should thoroughly research the requirements.