GSTR-3 is an important part of the Goods and Services Tax (GST) system, and businesses need to file it every month. It is like a summary that shows what a business sold, bought, and the taxes it owes. This form helps businesses match their sales and purchases, making sure they calculate taxes correctly and claim the right tax credits. GSTR-3 filing is crucial for businesses to be transparent and fulfill their tax responsibilities. It’s essential to understand GSTR-3 details to report accurately and avoid penalties from tax authorities. Also, don’t forget about other related keywords like GSTR-3B filing, GST 3 months return, and GSTR-3 return.

| Table of Contents |

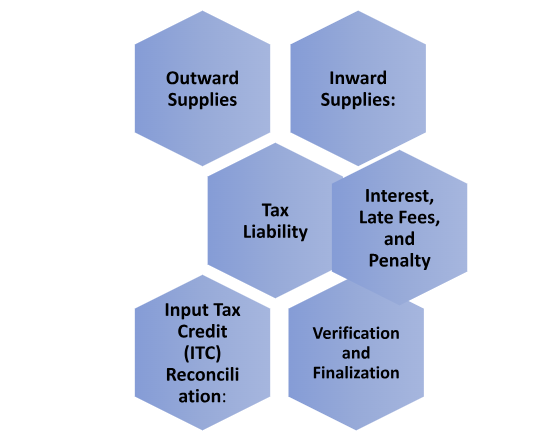

Components of GSTR-3 and their relevance

GSTR-3 consists of several components that play a significant role in the Goods and Services Tax (GST) compliance process. These components provide a comprehensive overview of a taxpayer’s tax liabilities, input tax credit (ITC) claims, and overall financial transactions. Here are the key components of GSTR-3 and their relevance:

- Outward Supplies: This section captures details of a taxpayer’s outward supplies of goods or services. It includes information such as the taxable value, tax rates, and taxes charged. Accurate reporting in this section ensures proper calculation and payment of GST on outward supplies.

- Inward Supplies: The inward supplies component focuses on capturing details of goods or services procured by the taxpayer. It includes information on purchases from registered suppliers, imports, and purchases liable for reverse charge. This section helps reconcile input tax credit (ITC) and ensures compliance with tax regulations.

- Input Tax Credit (ITC) Reconciliation: GSTR-3 allows businesses to claim ITC on their eligible purchases. This component facilitates the reconciliation between the taxpayer’s inward supplies and outward supplies, ensuring the correct utilization of ITC and reducing the chances of any discrepancies.

- Tax Liability: The tax liability section provides a summary of the taxpayer’s GST liability for the reporting period. It includes the tax payable on outward supplies, reverse charge liability, and any other applicable taxes. Accurate reporting in this component ensures proper payment of GST to the government.

- Interest, Late Fees, and Penalty: This component highlights any interest, late fees, or penalties levied on the taxpayer due to delayed or incorrect filing. Compliance with GSTR-3 filing deadlines and accurate reporting helps avoid unnecessary financial burdens.

- Verification and Finalization: The final section of GSTR-3 includes verification and declaration by the taxpayer, stating the accuracy and completeness of the information provided. This step ensures accountability and compliance with GST regulations.

Key documents required for GSTR-3 filing

When filing GSTR-3, businesses are required to provide specific documents. Here are the key documents typically required for GSTR-3 filing:

1.Inward Supplies (Purchases):

A. Purchase invoices: Valid tax invoices received from registered suppliers for goods or services purchased.

B. Import documents: Invoices, bills of entry, and other relevant customs documents for imported goods.

C. Documents related to reverse charge: Invoices and payment records for supplies liable for reverse charge, where the recipient is responsible for paying the tax.

2.Outward Supplies (Sales):

A. Sales invoices: Valid tax invoices issued to customers for goods or services supplied.

B. Export-related documents: Invoices, shipping bills, and other relevant documents for goods exported out of the country.

3.Input Tax Credit (ITC) Records:

A. Tax invoices: Invoices received from registered suppliers, containing the required details for claiming ITC.

B. Debit/credit notes: Records of debit or credit notes issued or received related to changes in the value or tax charged on inward supplies.

4.Bank Statements:

Bank statements reflecting transactions related to inward and outward supplies, including details of tax payments and refunds.

5.Payment-related Records:

Challans: Copies of challans or receipts for tax payments made to the government.

6.Purchase and Sales Registers:

Detailed registers or ledgers showing a record of all purchases and sales made during the reporting period.

7.Input Service Distributor (ISD) Records:

Documentation related to the distribution of input tax credit among different branches or units of a business, if applicable.

8.Other Supporting Documents:

Any additional supporting documents, such as delivery challans, transportation documents, contracts, agreements, or any other records that validate the transactions.

Procedure for filing GSTR-3

The procedure for filing GSTR-3 involves several steps that businesses need to follow to fulfill their Goods and Services Tax (GST) compliance requirements. Here is a general outline of the procedure:

- Log in to the official GST portal (www.gst.gov.in) using your valid credentials.

- Locate the “Returns Dashboard” and select the GSTR-3 filing section.

- Ensure that the details in your previously filed GSTR-1 (outward supplies) and GSTR-2 (inward supplies) are accurate and up to date. Make any necessary amendments or corrections if required.

- Auto-Population of Details: GSTR-3 is an auto-populated return based on the information provided in GSTR-1 and GSTR-2. Verify if the data from these returns has been populated correctly.

- Check the tax liability section and verify the calculated tax amounts based on the information provided. Review and update input tax credit (ITC) details, ensuring accuracy and compliance with GST rules.

- Check Interest, Late Fees, and Penalty: Verify if any interest, late fees, or penalties are applicable based on delayed or incorrect filing.

- Validate the GSTR-3 return to ensure all mandatory fields are filled correctly. Submit the return electronically using the digital signature certificate (DSC) or electronic verification code (EVC) method.

- Acknowledgment and ARN: Once the return is successfully submitted, an acknowledgment reference number (ARN) will be generated. Note down this number for future reference.

- Payment of Tax: If there is any tax liability after adjusting input tax credit, make the payment through the appropriate mode (online or offline) using the GST portal.

Compliance for GSTR-3 filing

Compliance for GSTR-3 filing is crucial for businesses to meet their obligations under the Goods and Services Tax (GST) regime. GSTR-3 serves as a consolidated return that summarizes a taxpayer’s outward supplies, inward supplies, and tax liabilities. Here’s why compliance with GSTR-3 filing is essential:

- Avoid Penalties: Non-compliance or delayed filing of GSTR-3 can attract penalties, late fees, and interest charges. By complying with the filing deadlines, businesses can avoid unnecessary financial burdens.

- Input Tax Credit (ITC) Claims: Accurate and timely GSTR-3 filing ensures the correct claiming of input tax credit. Failing to comply may result in the loss of eligible ITC, impacting the cash flow and profitability of the business.

- Transparency and Accountability: Compliance with GSTR-3 filing promotes transparency in business operations and enhances credibility with tax authorities. It demonstrates a commitment to maintaining accurate financial records and following the GST regulations.

- Legal Compliance: GST laws mandate the filing of GSTR-3 by registered taxpayers. By complying with the filing requirements, businesses fulfill their legal obligations, reducing the risk of legal consequences and audits.

- Seamless Business Operations: Regular and timely GSTR-3 filing enables businesses to maintain accurate records, reconcile transactions, and plan effectively. It streamlines the compliance process and minimizes disruptions to day-to-day operations.

Addressing common errors and mistakes in GSTR-3 filing

Here are some common errors and mistakes that businesses should address to avoid issues during the filing process:

1.Incorrect Reporting of Outward Supplies:

A. Ensure that all outward supplies are accurately reported, including correct taxable values, tax rates, and tax amounts.

B. Double-check that the HSN/SAC codes (Harmonized System of Nomenclature/Services Accounting Code) are correctly mentioned for each item.

2.Inaccurate Reporting of Inward Supplies:

A. Verify that all inward supplies, such as purchases and imports, are correctly reported with accurate invoice details.

B. Cross-check the input tax credit (ITC) claimed against valid tax invoices received from registered suppliers.

3.Failure to Include All Relevant Transactions:

A. Review all business transactions and ensure that no sales, purchases, or other taxable supplies are missed in the GSTR-3 filing.

B. Include all inter-state supplies, exports, and supplies liable for reverse charge, where applicable.

4.Errors in Input Tax Credit (ITC) Reconciliation:

A. Reconcile the ITC claimed with the information available in the GSTR-2A (auto-populated from suppliers’ GSTR-1).

B. Rectify any discrepancies, including missed or mismatched invoices, to avoid incorrect reporting of ITC.

5.Non-Compliance with Timelines:

A. Adhere to the prescribed due dates for GSTR-3 filing to avoid penalties or late fees.

B. Set up reminders and establish a process to ensure timely submission of the return.

6.Incorrect Utilization of ITC:

A. Ensure that the ITC is utilized correctly against the tax liabilities in the appropriate manner (e.g., Integrated Tax, Central Tax, State/UT Tax, Cess).

B. Cross-verify the utilization of ITC against the tax liability calculated for each component.

7.Data Entry and Calculation Errors:

A. Carefully enter data into the appropriate fields in GSTR-3 to minimize mistakes.

B. Utilize GST-compliant accounting software to automate calculations and reduce human errors.

8.Lack of Reconciliation with Books of Accounts:

A. Regularly reconcile GSTR-3 data with the books of accounts to identify and rectify any discrepancies.

B. Reconcile sales, purchase, and financial records to ensure consistency and accuracy.

Conclusion

Accurate and timely filing of GSTR-3 is crucial for businesses to comply with Goods and Services Tax (GST) regulations and maintain transparency in their financial transactions. By addressing common errors and mistakes during the filing process, businesses can avoid penalties, interest charges, and potential audits by tax authorities. It is essential to pay attention to details, such as reporting outward supplies and inward supplies accurately, reconciling input tax credit (ITC) claims, and adhering to filing timelines. Furthermore, businesses should utilize GST-compliant accounting software, maintain up-to-date records, and reconcile GSTR-3 data with their books of accounts. By taking these measures, businesses can ensure compliance, claim eligible ITC, and streamline their GST reporting. Seeking professional advice and staying updated with the latest GST regulations can further assist businesses in avoiding errors and ensuring a smooth and accurate GSTR-3 filing process. Overall, by prioritizing accuracy and compliance, businesses can successfully meet their GST obligations and contribute to a seamless tax ecosystem.