Non-Banking Financial Companies (NBFCs) in India have emerged as crucial players in the financial sector, serving the diverse financial requirements of individuals and businesses. As India’s economy constantly evolving and digital transformation reshapes the financial paths. The future of NBFCs in India holds immense potential and promise. In this article, we explore the future of NBFCs in India, delving into the role of advanced technology, regulatory dynamics, and adopting inclusive growth.

| Table of Content |

Short Note on NBFCs

NBFCs full form is Non-Banking Financial Companies, which are financial institutions that offer a wide range of banking and financial services in India. While they don’t hold a banking license, still play a vital role in expanding access to credit and financial services, mainly to understand the underserved part of the population. It offers services like wealth management, insurance-related activities, investment, asset financing, lending, and microfinance.

One of the key features of NBFCs is their flexibility in lending and customer service. They often cater to customers who may not meet the strict requirements of traditional banks, providing loans and financial products to individuals and businesses with limited collateral or credit history. NBFCs are known for their ability to customize lending products and offer quick processing times, making them a preferred choice for many borrowers.

NBFCs have contributed significantly to financial inclusion in India by reaching out to rural and semi-urban areas where traditional banks may have a limited presence. They bridge the credit gap and help in the development of sectors like agriculture, small businesses, housing, and microfinance.

However, NBFCs in India operate under regulatory oversight from the Reserve Bank of India (RBI) and must adhere to specific guidelines and regulations to maintain financial stability and protect consumer interests. They are required to maintain a minimum level of capital adequacy, ensure corporate governance standards, and comply with reporting and disclosure norms.

Significance of NBFCs in the Indian Economy

Here are some key aspects highlighting their significance:

- Financial Inclusion: NBFCs play a crucial role in promoting financial inclusion by providing access to credit and financial services to underserved segments of the population. They reach out to individuals and businesses in remote areas, small towns, and rural regions where traditional banks may have limited presence.

- Credit Accessibility: NBFCs complement the banking sector by expanding the availability of credit in the economy. They offer a diverse range of financial products such as NBFCs loan are personal loans, vehicle loans, microfinance, housing finance, and small business loans. This enables individuals and businesses to fulfil their financial requirements, such as starting a business, purchasing assets, or meeting personal expenses.

- Sectoral Focus: NBFCs cater to specific sectors that may have unique financing needs or face challenges in obtaining credit from traditional banks. For example, NBFCs specializing in agriculture finance provide credit to farmers and agribusinesses, addressing the specific requirements of the agricultural sector.

- Job Creation and Economic Growth: The growth of NBFCs has a positive impact on job creation and economic growth. As NBFCs expand their operations, they create employment opportunities across various roles such as sales, customer service, credit assessment, risk management, and administration.

- Regional Development: NBFCs often operate in regions with limited banking infrastructure. Their presence in these areas fosters regional development by channelling credit and financial services to local businesses and individuals. This promotes entrepreneurship, income generation, and economic activity, leading to the overall development of these regions.

Role of Advanced Technology in the Future of NBFCs

Advanced technology is poised to play a transformative role in shaping the future of NBFCs. Here are some key areas where technology is expected to have a significant impact:

- Digital Transformation: NBFCs are increasingly embracing digital transformation to streamline their operations, enhance customer experience, and improve efficiency. Technology enables the automation of various processes, such as loan origination, underwriting, documentation, and customer onboarding. By digitizing these processes, NBFCs can reduce paperwork, enhance turnaround times, and provide seamless and convenient services to customers.

- Digital Lending Platforms: Technology-driven lending platforms are revolutionizing the lending landscape. Online platforms and mobile applications enable borrowers to apply for NBFCs loans, submit documents, and track their application status digitally. Advanced algorithms and data analytics are used for credit assessment, risk profiling, and determining loan eligibility. These platforms also facilitate peer-to-peer lending and crowdfunding, creating new avenues for borrowers and investors to connect.

- Data Analytics and Artificial Intelligence (AI): NBFCs are leveraging data analytics and AI to gain insights, make informed decisions, and enhance risk management. Advanced analytics models analyse vast amounts of data to identify creditworthiness, predict defaults, and assess market trends. AI-powered chatbots and virtual assistants are employed for customer service, resolving queries, and providing personalized recommendations. These technologies enable NBFCs to streamline operations, improve customer engagement, and mitigate risks.

- Robotic Process Automation (RPA): Robotic Process Automation automates repetitive and rule-based tasks, freeing up human resources for higher-value activities. NBFCs can leverage RPA to automate tasks like data entry, document verification, and report generation. This not only reduces manual errors but also improves operational efficiency, reduces costs, and enhances process scalability.

- Biometric Authentication and Security: Advanced technology facilitates secure and seamless customer authentication. NBFCs are adopting biometric authentication methods such as fingerprints, facial recognition, and voice recognition for identity verification and secure access to financial services. These technologies enhance security, reduce fraud, and provide a convenient user experience for customers.

- Blockchain and Smart Contracts: Blockchain technology offers secure, transparent, and tamper-proof transaction records. NBFCs can leverage blockchain for secure loan disbursement, verification of collateral, and creating immutable audit trails. Smart contracts, built on blockchain, enable self-executing and self-enforcing agreements, reducing the need for intermediaries and streamlining processes.

- Open Banking and API Integration: NBFCs can collaborate with fintech firms and banks through open banking and Application Programming Interfaces (APIs). Open banking allows the secure sharing of customer data and facilitates integration between different financial service providers. By leveraging APIs, NBFCs can access customer data, credit information, and financial infrastructure, enabling seamless interoperability and enhancing the range of services offered.

Potential Trends and Dynamics that Shape the Future of NBFCs in India

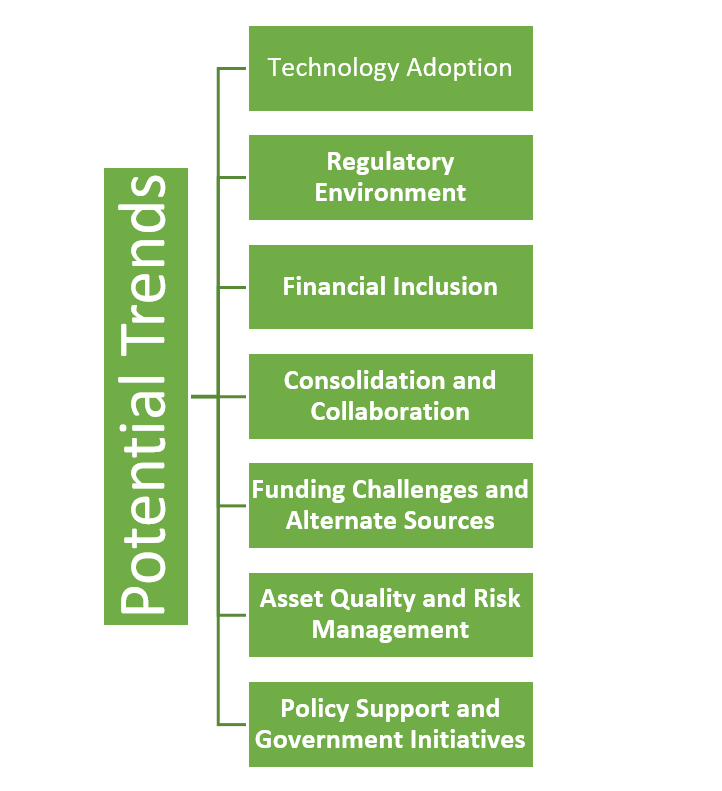

The future of NBFCs in India holds both opportunities and challenges. Here are some potential trends and dynamics that could shape the future of NBFCs in India:

- Technology Adoption: NBFCs are likely to continue leveraging technology to enhance their operational efficiency, customer experience, and risk management capabilities. This includes embracing digital lending platforms, using data analytics for credit assessment, and implementing advanced technology solutions for process automation and customer service. The adoption of technology will enable NBFCs to reach a wider customer base, reduce costs, and improve the speed and accuracy of their services.

- Regulatory Environment: The RBI is expected to maintain its focus on strengthening the regulatory framework for NBFCs. The regulatory scrutiny is likely to continue, with an emphasis on risk management, corporate governance, capital adequacy, and consumer protection. The RBI may introduce new guidelines and regulations to address emerging risks and ensure the stability of the financial system. Compliance with regulatory requirements will be crucial for NBFCs to maintain their operations and sustain growth.

- Financial Inclusion: NBFCs play a vital role in providing financial services to underserved and unbanked segments of the population. The future of NBFCs in India is likely to witness a continued focus on financial inclusion, with efforts to expand their reach to rural and semi-urban areas. Government initiatives such as Jan Dhan Yojana, Pradhan Mantri Mudra Yojana, and affordable housing schemes will create opportunities for NBFCs to cater to the financial needs of these segments.

- Consolidation and Collaboration: The NBFC sector in India is expected to witness consolidation, as larger NBFCs acquire smaller players to gain market share, expand their product offerings, and achieve economies of scale. Additionally, partnerships and collaborations between NBFCs, banks, and fintech companies are likely to increase, enabling synergies and innovative solutions. Collaborative efforts can help NBFCs diversify their offerings, enhance their digital capabilities, and tap into new customer segments.

- Funding Challenges and Alternate Sources: Access to funding has been a key challenge for NBFCs, particularly after the liquidity crunch in the sector. In the future, NBFCs may explore alternate sources of funding, such as securitization, issuance of bonds, and foreign investments. Diversification of funding sources will help NBFCs reduce dependency on traditional banking channels and improve their financial stability.

- Asset Quality and Risk Management: As NBFCs expand their lending activities, maintaining robust risk management practices and ensuring good asset quality will be essential for their sustainability. NBFCs will need to adopt stringent credit assessment processes, monitor their loan portfolios effectively, and implement proactive risk mitigation measures. Strong risk management frameworks and adequate capital buffers will be critical to navigating any potential economic downturns or asset quality challenges.

- Policy Support and Government Initiatives: The Indian government has been taking various measures to support the growth of NBFCs, including facilitating refinancing mechanisms, providing liquidity support, and introducing stimulus packages during challenging times. Continued policy support and government initiatives will play a significant role in shaping the future of NBFCs, ensuring a conducive environment for their operations and growth.

Takeaway

Through the above-mentioned information, it can be said that the future of NBFCs in India holds tremendous potential for growth, innovation, and inclusive development. As the Indian economy continues to evolve, NBFCs are adapting to emerging trends and leveraging advanced technologies to transform their operations and enhance customer experiences. Furthermore, regulatory reforms and policies are ensuring the stability and sustainability of the NBFC sector. Regulators are emphasizing compliance, risk mitigation, and governance frameworks, which in turn foster consumer protection and financial stability.